The 2018 stock market crash is now a fait accompli, having taken a polar bear plunge that put ice in the veins of the Fed and electrified their collective spine with such a deep chill they ran like a fat walrus from the bear market to halt their long-nurtured plans of economic tightening. With that event fulfilled, I’m now predicting a 2019 recession as the major economic news for this year (both US and global).

To confirm my bearish claim on the market’s crash:

Several leading stock market indexes around the globe endured bear market declines in 2018. In the U.S. in December, the small cap Russell 2000 Index (RUT) bottomed out 27.2% below its prior high. The widely-followed U.S. large cap barometer, the S&P 500 Index (SPX), just missed entering bear market territory, halting its decline 19.8% below its high.

But the Dow fell into bear territory and the NASDAQ even further into the bear’s territory.

In terms of real cost, anyone who scoffed at my 2018 warnings and held through 2018 is still recovering from his or her losses. That we have only just this week recovered those losses is quite easily proven with one simple graph of 2018 where the action begins in January where I said it would and hits full crash velocity in the fall:

If you like wild financial roller coaster rides that end right back where you started, stocks were the place to be in 2018. Obviously, it was an extremely bumpy ride to worse than nowhere for those who bought and held in the market thoughout 2018. The year was, however, a completely pleasant financial ride for those who were in cash all year, which was the only major asset that performed positive for the year! (And, of course, if you are the rare prodigy who can accurately time every peak and every trough, years of high volatility can make you more money than a steady climb; but then you are a very rare bird with a very high tolerance for risk — some would say a fantasy.)

I can attest to the calm because that is where I sat out the turbulence, being someone who doesn’t prefer bumpy rides to worse than nowhere. Moreover, those who jumped out at January’s peak, as I did, and remained out of stocks for the rest of the year, could also have experienced a joy ride of pure gains over the past three months in the stock market, instead of waisting the whole rally on mere loss recovery.

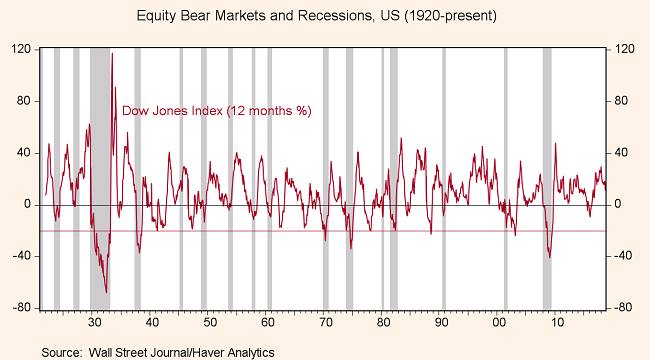

Now the losses are finally made up, and so reported here, but that doesn’t diminish the risk of a 2019 recession. On the contrary, US stock market crashes usually correspond with a recession, but often happen before or after the recession:

In the US, most analysts agree that bear markets and domestic recessions have generally been fairly closely related, though the exact leads and lags between the two may differ considerably across cycles. Furthermore, there have been several bear markets, notably in 1987 and 1978, that have not been accompanied by recessions, and vice versa.

That is not to say the stock market will make it back up to its record summit ( or not go deeper into its polar region than in December; but, whether it does or not, a 2019 recession is in the making.

What will spark the next bear market? An economic recession, or the anticipation of one by investors, is a classic trigger, but not always. Another trigger has been a sharp slowdown in corporate profit growth, as we are seeing now…. Stock market pundits are widely divided about the nature of the next bear. For example, Stephen Suttmeier, the chief equity technical strategist at Bank of America Merrill Lynch, has said he sees a “garden-variety bear market” that will last only six months, and not go much beyond a 20% dip, per CNBC. At the other end of the spectrum, hedge fund manager and market analyst John Hussman has been calling for a cataclysmic 60% rout.

Whatever continues to play out in the stock market, the main economy now steps into the forefront of the picture for me. The stock market’s 2018 trip on the Polar Bear Express already did its damage to investor confidence and pushed fleeing money into bonds, bringing long-term bond interest down, even as the Fed was dumping bonds, which should, otherwise, have pushed interest up. (After all, the Fed bought bonds in the first place to lower long-term interest.) That changed the bond market significantly enough to decisively align with recessionary sentiment in a historic bond inversion. And that makes 2018’s bear market a game changer.

While bond-market inversion has never failed at predicting a recession in the last half century, that is not, by any means, the only reason I’m predicting a 2019 recession, which I did before the full inversion. I laid out in my first Premium Post the numerous headwinds that would likely assail the US and global economies in 2019, regardless of anything that happens in stocks. So, my attention this year moves along to those things and to the likelihood of a 2019 recession hitting around summertime (as noted before not to be officially declared until half a year after that because that is just a fact of how recessions are declared — always more than half a year after they start as we wait for the stats to come in).

We may well see a second crash in US stocks because of this year’s recession, but whether we do or not is irrelevant now that we have already taken a trip with the bear. Another game-changing result of that excursion into the polar regions that happened because of the Federal Reserve’s Great Rewind is that it proved to everyone the Fed cannot do what it has always said it could (and I always said it couldn’t), which was to reduce its balance sheet and return to normal interest targets after building a fake (as in unsustainable) recovery. Therefore, confidence in the Fed is also badly shaken, leaving it weaker in its ability to lift us out of a 2019 recession than its bloated balance sheet and already-low interest rates leave it. At this time, the Fed’s moves are just following the market’s dictates. The Fed is now the market’s bitch in nearly everyone’s eyes.

Moreover, the Fed’s damage to the economy is still coming in. I’ve noted before that there is typically a half-year lag between any major Fed action and where the economy goes; yet, the Fed is continuing to reduce its balance sheet by the same amount this month and next, cutting that by half in June but not stopping until the end of summer. That means there will be half a year of lagging results after this summer, even as the Fed’s actions from this past winter are still playing out into this summer. So, there is plenty of downdraft still to carry through the general economy all the way to the end of this year as a result of the Fed’s recent and continuing actions.

My past statements about the next major economic downturn have always said the Great Recession will return like the undead because the Fed will go too far in sucking liquidity out of the economy. I believe the Fed has already done that, but the results of that withdrawal will take time to become fully realized. That’s why President Trump and his two stooges of finance are begging the Fed to go back to QE “immediately” because, if they wait until it is obviously necessary, it will be WAY too late!

You see, any results from the Fed jumping back into full economic-stimulus mode — if the Fed does as the Trump administration demands and as most financial analysts and investors now appear to expect — will also take time to be realized … other than in stocks and bonds. Moreover, any results they do get will have diminished returns at best. At worst, new Fed stimulus will now have an opposite effect if people are smart enough to realize it all means we are right back where we started and that Fed money–printing must now go on ad nauseam. So, the Fed has done its damage (which it really did by the recovery path it chose), and the bond market knows it. For stocks, as I laid out in that first Premium Post, this will be a year of turmoil whether stocks are generally up or down.

Now on to the talking points throughout the past week’s news that show we are, as I’ve claimed, goose-stepping our way into a 2019 recession as metrically as the ticking of a coo coo clock:

Tick tock goes the clock, counting down to a 2019 recession

The U.S. private sector added 129,000 jobs in March, the weakest reading in 18 months and below consensus expectations of 165,000, according to an Econoday economists survey. The report is watched for clues to official labor data due Friday.

New hirings around 120k or less are usually recessionary.

Following last month’s weak ADP print which front-ran the dismal “must be an outlier due to weather, shutdown, or anything else” payrolls data, expectations were for a slightly weaker ADP employment headline in March. However … ADP disappointed, adding just 129k jobs in March (well below the expected +175k…. This is the weakest growth in employment since Sept 2017.

On the other hand …

The BLS reported that the US added 196K payrolls in March, higher than the 177K.

Since the job reports are all over the place, it’s hard to know who to believe — the ADP or the government’s Bureau of Lying Statistics. You may recall that February’s jobs came in at an extremely disappointing 20k, which the BLS just revised upward to an almost equally disappointing 33k. To sort out the messy disagreement in job statistics, consider the following for the BLS’s more optimistic numbers: If you average all three months of the first quarter, 2019 is down from 2018’s average for the first quarter by a fairly significant 40,000 jobs per month. Annualized, that would be the lowest level in almost five years! So, even the better BLS numbers are not the numbers you want to see if you believe the Trump Tax Cuts and government hyperspending — now in effect for more than a year — are taking the economy upward! Kocain Kudlow must have lasting damage from his old habit in order to call this a strong economy, even as he begs for more immediate Fed assistance. No wonder he’s begging!

Meanwhile 2019’s rise in continuing jobless claims is the worst we’ve seen since the start of the Great Recession!

The overall unemployment rate just started trending back up as well:

Those little upticks at the end of each graph may seem insignificant, but they are actually highly significant because the first uptick in unemployment downtrends from a low bottom always immediately precedes a recession:

That means two of the most accurate predictors of recession, according to the Fed — yield-curve inversions and unemployment trend changes — are now lined up on the same side for a 2019 recession.

On average, since 1969, the unemployment rate trough occurred nine months before the NBER-determined recession trough, while the yield curve inversion occurred 10 months before…. The minimum lead times were one month for the unemployment trough and five months for the yield curve inversion.

On the downside of the above jobs report, wages (which had been seeing a little better improvement, albeit briefly) fell off badly to just a 0.1% gain. Manufacturing jobs within this report also dropped significantly; so, on to manufacturing statistics of the week just passing …

Markit’s March services purchasing managers index [PMI] came in at 55.3 above consensus expectations of 54.8, according to FactSet. A reading of at least 50 indicates improving conditions.

Pretty good except …

US Manufacturing PMI dropped to weakest since June 2017

So, services up but manufacturing well down … and …

The Institute for Supply Management’s services sector gauge fell to 56.1% in March, down from 59.7% in February.

A broad slide in manufacturing — as verified in both the jobs report and the PMI — is more likely to bring a 2019 recession than the converse rise in health-care and education jobs is likely to bring economic salvation.

Moreover …

In a world where Caterpillar is considered a global industrial bellwether and a key indicator of economic inflection points … today’s downgrade of Caterpillar by Deutsche Bank is a harbinger that the recent risk on euphoria may be coming to an end….. Dilllard says that “synchronized global growth has collapsed, the China Land Cycle is rolling over (and will continue to weaken despite the single positive data point this week), Europe is slowing more than expected and the US is oversaturated with construction equipment…. Together this synchronized slowdown will not only usher in a negative earnings revision cycle, but also make 2019 the cyclical peak.

Then again …

The Financial Times reported that the U.S. and China were nearing the final stages of trade talks (paywall) and had two issues left to resolve—the current tariffs on Chinese imports and details on an enforcement mechanism to keep China compliant with the deal.

US stocks jumped euphorically this week upon China’s PMI (manufacturing index) getting a mild bump; but, in fact, a rise to 50.5 is not considered expansionary for China’s economy, but merely flat; and that tiny bump came after a huge one-off bump in credit by the People’s Bank of China, now mostly used up.

Meanwhile, other Asian countries are fully in a manufacturing contraction. PMI throughout European nations also continued to plummet.

Autos, retail and housing continue to sputter “2019 recession”

Auto sales in the U.S. wrapped up an ugly first quarter with dismal results for the month of March as the buying frenzy from last year’s tax cuts wore off and the economy continues to decelerate…. General Motors saw deliveries drop 7% for the quarter, with all four brands falling…. Fiat Chrysler sales fell 7.3%…. Ford sales were down 5% in March….

All other major manufacturers with plants in the US were down, except Honda. Even pickup sales — a formerly hot performer — are sputtering.

Another area where the jobs report fell off was in retail. Only two periods in retail sales looked as bad as the presen — the dot-com crash and the Great Recession crash:

And that is including online sales!

One more higbly accurate indicator the Fed gives for timing a recession is a decline in housing:

Housing downturns have preceded every U.S. recession since World War II. For example, one measure of the momentum of residential investment turned negative before each of these episodes…. Recent movements in several housing indicators—mortgage rates, existing home sales, real house prices and the momentum of residential investment—resemble those seen in the late stages of past economic expansions. Could these storm clouds gathering over the housing market be signaling a broader economic downturn in 2019 or 2020….? Each of these indicators is in a range that, in previous cycles, preceded a recession by a year or two.

The hottest housing markets are still cooling, which doesn’t bode well for jobs in construction either (where job growth remained moderate in the latest reports):

Listing prices are declining in what were some of the hottest housing markets in the country…. For instance, the median asking price in San Jose, California, was $1,100,050 in March – the highest of 500 metro areas, but down 11.6% from a year ago. Median asking prices in Denver and Boulder, Colorado, experienced similar declines. The median asking price declined the most year over year in Lynchburg, Virginia, plunging 37% to $145,000. Overall, 114 of the 500 markets Realtor.com surveyed saw a drop in the median listing price. On the other side, smaller markets in the middle of the county experienced the largest increases in asking prices.

This is all just this week’s news!

Elsewhere, the Canadian housing market is falling hard (just a fun fyi, not that it has anything to do with a US recession … but certainly fits the picture of a simultaneous global recession:

The Real Estate Board of Greater Vancouver (REBGV) reported today … the lowest sales total for [March] since 1986 – down 31% from a year earlier and 46% below the 10-year March sales average.

And Australia’s is looking precarious:

Australia’s housing boom/bubble could unravel badly. Last week, Grant Williams highlighted a video by economist John Adams, Digital Finance Analytics founder Martin North, and Irish financial adviser Eddie Hobbs, who say Australia’s economy looks increasingly like Ireland’s just before the 2007 housing collapse.

Elsewhere on the global recessionary front, German industrial orders just took a slam to a level Germany hasn’t seen since the Great Recession, and Germany can always be counted on as doing better than any other part of the EU:

Germany estimates that, if Brexit doesn’t happen neatly, Germany’s own numbers will get much worse.

On the other hand …

Global recession fears are exaggerated and … a recovery is most likely in store for both China and the Eurozone in the next several months.

Sure. And what was this bit of good news based on?

While the financial media continue to fret over the global slowdown, a salient piece of good news having positive economic implications was largely ignored…. The good news is that at the end of the first quarter last week, the S&P 500 Index registered its best start to a year since 1998…. In years when the SPX was up strongly and didn’t suffer a significant decline in the first three months, it nearly always finished higher at the end of the year.

Yeah, that’ll do it. We’re safe from a recession in 2019 now. You can all go back to sleep. However, bear in mind, that assurance comes from a permabull who calls last year’s stinging bear market “a 20% correction,” making him, I think, the only person on earth who defines a 20% plunge that radically changes the course of the Fed and sets up a bond inversion as a “correction.” That man is from mars.

Why we NEED a 2019 recession

I am reasonably confident the few people (if not the only person) who mocked my prediction of a stock market crash in 2018 and of a housing downturn, both of which hit on every beat throughout the year, aren’t going to do any better betting against me on a 2019 recession.

I know that sounds smug, but here’s why I don’t care: I like to taunt them into trying to because, when this all proves out just as 2018 proved out, it all goes to demonstrate that the massive failure of the Fed’s fake recovery was as predictable as I’ve always said. The Fed’s plan is going to fail; it was always obvious it was going to fail; and it is now, in fact, failing in exactly the manner I’ve said it would.

What I really want to do is utterly destroy the Federal Reserve’s unmerited credibility and, with that, its centralized planning and manipulation of the global economy as well as its rigging of stock and bond markets. I want to see Capitalism rise again from the Fed’s ashes. To that more important goal, I think a big, fat recession in 2019 could be the best thing that every happened, even though it would be the worst thing that ever happened.

So, bet on the Goliath Fed, or bet on this little David. The Federal Reserve went down hard last year even as each of my little stones hit their mark (stock-market crash, Carmageddon, Retail Apocalypse, and Housing downturn). So, the Fed bears some disgrace by lying flat on its face already. Now, it’s time to cut off its head, which it will do for me when the 2019 recession starts to undo the whole well-Fed world, and Father Fed is helpless to prevent it.

This article was originally published at The Great Recession blog. It is re-printed here with permission. Liked it? Take a second to support David Haggith on Patreon!